By Author Devanssh Mehta | Industry Intelligence Report

Executive Summary

India’s oncology market has moved from being a niche specialty healthcare segment into one of the most strategically important components of the national healthcare economy. Cancer is no longer viewed solely as a medical challenge—it has become a public health, pharmaceutical, infrastructure, policy, technology, insurance, and socioeconomic issue.

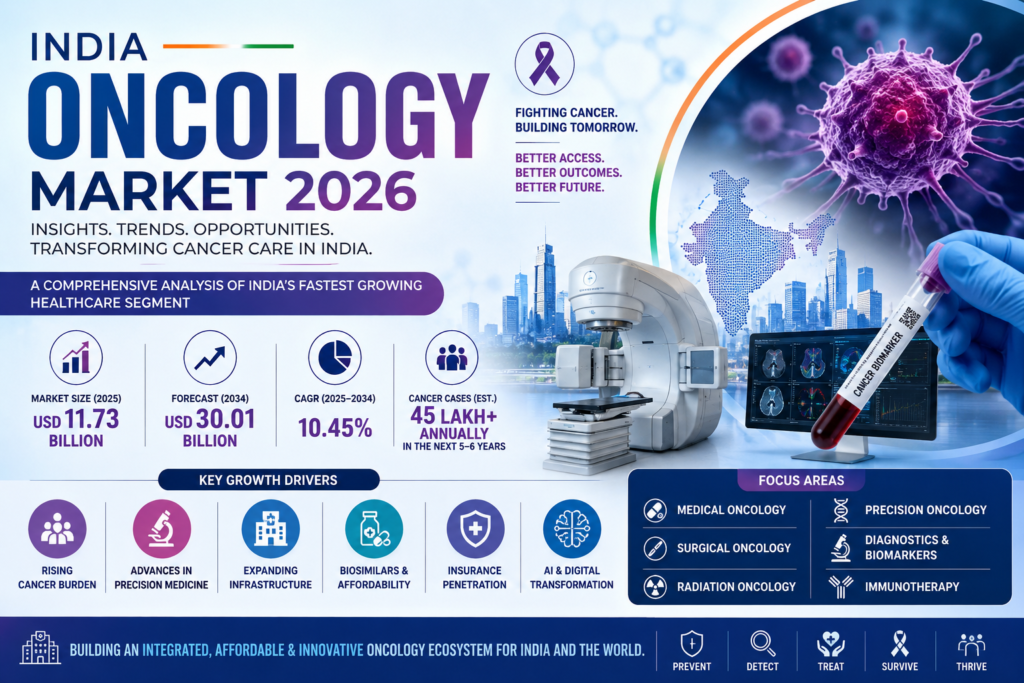

Current estimates place India’s oncology market at approximately USD 11.7 billion in 2025, with projections reaching nearly USD 30 billion by 2034, implying sustained double-digit growth. (IMARC Group) Across narrower oncology segments, growth rates remain even stronger, with some industry analyses forecasting oncology market expansion approaching 20% CAGR through 2030. (Research and Markets)

Simultaneously, India is witnessing a structural cancer burden transition. Estimates suggest the country may move toward 45 lakh annual cancer cases within the coming five to six years if current trends continue, creating extraordinary demand for diagnostics, therapeutics, radiation services, precision medicine, and survivorship ecosystems. (EY)

This report evaluates:

- Market size and structure

- Demand and epidemiology

- Competitive dynamics

- Therapeutics and technology shifts

- Precision oncology and AI

- Investment opportunities

- SWOT and PESTLE analysis

- Future outlook to 2035

1. Introduction: Oncology as India’s Next Healthcare Growth Engine

India’s healthcare evolution has historically passed through multiple phases:

- Infectious disease control

- Maternal and child healthcare expansion

- Cardiometabolic disease management

- Specialty care development

- Precision medicine emergence

Today, oncology occupies the center of healthcare transformation.

Cancer treatment in India has become one of the fastest-expanding healthcare categories because of:

- Rising longevity

- Urbanization

- Environmental exposure

- Better screening

- Increased affordability

- Expansion of tertiary care infrastructure

- Growth of insurance penetration

- Biosimilar availability

The oncology ecosystem now extends far beyond chemotherapy.

Modern oncology includes:

- Prevention

- Screening

- Diagnostics

- Surgical oncology

- Radiation oncology

- Medical oncology

- Immunotherapy

- Precision medicine

- Survivorship care

- Digital monitoring

2. Indian Oncology Market Size and Growth Outlook

Different methodologies produce different estimates depending on scope (therapeutics only vs full oncology ecosystem).

Indicative estimates:

| Segment | Estimated Size |

|---|---|

| Total India Oncology Market (2025) | USD 11.73 Billion |

| Forecast (2034) | USD 30.01 Billion |

| CAGR | 10.45% |

Alternative market models estimate oncology expansion of approximately USD 2.35–2.36 billion incremental opportunity during 2025–2030 with growth near 20% CAGR. (Research and Markets)

Drug-specific oncology estimates indicate:

| Segment | Market Estimate |

|---|---|

| Oncology Drugs Market (2025) | ~USD 6.21 Billion |

| Share of Global Market | ~2.4% |

These differences indicate that oncology in India should be viewed as a layered market rather than a single industry.

3. Epidemiological Foundation of Oncology Growth

Market expansion is fundamentally demand-driven.

Cancer incidence growth reflects:

Demographic Drivers

- Aging population

- Increased life expectancy

Lifestyle Drivers

- Tobacco use

- Sedentary behavior

- Obesity

- Alcohol consumption

Environmental Drivers

- Air pollution

- Occupational carcinogens

Biological Drivers

- Genetic predisposition

India documented approximately 1.46 million cancer cases in 2022 according to cancer registry references cited by market analyses, while broader estimates suggest under-reporting remains substantial. (Coherent Market Insights)

High-burden cancers include:

- Breast

- Lung

- Cervical

- Oral

- Colorectal

- Prostate

- Ovarian

- Leukemia

4. Market Segmentation Analysis

A. Medical Oncology

Largest revenue contributor.

Includes:

- Chemotherapy

- Targeted therapy

- Hormonal therapy

- Immunotherapy

Drivers:

- Hospital expansion

- Increased specialist availability

- Biosimilar adoption

Cancer therapeutics remain among the strongest growth categories in Indian pharma. (MarkNtel Advisors)

B. Surgical Oncology

Evolution areas:

- Robotic surgery

- Organ preservation

- Image-guided procedures

Demand growth is particularly visible in metro and tier-2 tertiary centers.

C. Radiation Oncology

Radiation infrastructure remains underpenetrated relative to disease burden.

India radiation oncology estimates:

| Metric | Value |

|---|---|

| Revenue (2025) | USD 310 Million |

| Forecast (2033) | USD 907 Million |

| CAGR | 14.4% |

Radiotherapy devices alone are projected to grow from approximately USD 165.7 million in 2025 to USD 384.1 million by 2034. (IMARC Group)

D. Precision Oncology

Precision oncology represents India’s highest-value future segment.

Precision oncology market estimates:

| Metric | Value |

|---|---|

| Revenue (2024) | USD 4.36 Billion |

| Forecast (2030) | USD 8.90 Billion |

| CAGR | 12.6% |

Technologies include:

- NGS

- Molecular profiling

- Companion diagnostics

- AI pathology

- Liquid biopsy

5. Indian Oncology Value Chain

The oncology value chain includes:

Research

↓

Diagnostics

↓

Treatment selection

↓

Drug procurement

↓

Hospital administration

↓

Monitoring

↓

Long-term follow-up

Major revenue pools:

- Pharmaceuticals

- Hospitals

- Diagnostics

- Devices

- Digital platforms

- Insurance

6. Pharmaceutical Transformation in Oncology

India’s pharmaceutical industry increasingly sees oncology as a strategic category.

Three therapy generations dominate:

Generation I

Traditional chemotherapy

Generation II

Targeted therapy

Generation III

Immunotherapy

Emerging:

Generation IV

Cell and gene oncology

Cancer treatment drug markets in India are projected to expand at approximately 12.2% CAGR through 2030. (MarkNtel Advisors)

7. Biosimilars: India’s Competitive Weapon

India’s oncology affordability story increasingly depends upon biosimilars.

Advantages:

- Lower cost

- Wider access

- Domestic manufacturing

- Reduced dependence

Strategic opportunities include:

- Monoclonal antibodies

- Growth factors

- Immunotherapies

8. Diagnostics Revolution

Cancer diagnosis increasingly drives treatment economics.

Growth segments:

- Molecular diagnostics

- Digital pathology

- Biomarker testing

- Liquid biopsy

- AI imaging

Diagnostics are becoming the fastest-growing precision oncology component. (Grand View Research)

9. Healthcare Infrastructure and Delivery

India’s oncology infrastructure shows major imbalance.

Challenges:

- Urban concentration

- Specialist shortages

- Long wait times

Positive developments continue through public–private expansion and regional cancer centers.

Examples of oncology service scale expansion are visible in tertiary institutions where patient registrations and treatment volumes have multiplied over recent years. (The Times of India)

10. Insurance and Affordability Dynamics

Key payment sources:

- Out-of-pocket

- Government insurance

- Private insurance

- Employer coverage

Affordability remains decisive.

Examples of innovative state programs show anti-cancer medicines being delivered at deep discounts through public initiatives. (The Times of India)

11. Investment Landscape

Investment hotspots:

High Opportunity

★★★★★ Precision Oncology

★★★★★ Biosimilars

★★★★★ Radiation Networks

★★★★★ AI Diagnostics

★★★★ Oncology Hospitals

★★★★ Genomics

12. Competitive Landscape

Participants include:

- Global pharma

- Domestic pharma

- Hospital chains

- Device manufacturers

- Diagnostics firms

International companies continue expanding oncology portfolios in India, including renewed entry into precision oncology categories. (The Economic Times)

13. Technology Disruption

Major disruptors:

Artificial Intelligence

- Imaging

- Decision support

Digital Oncology

- Remote monitoring

Robotics

- Precision surgery

Data Platforms

- Real-world evidence

14. SWOT Analysis

Strengths

- Large patient pool

- Strong pharma manufacturing

- Biosimilar capability

- Skilled clinicians

Weaknesses

- Unequal access

- Specialist shortages

- Cost burden

Opportunities

- Precision medicine

- Export leadership

- Medical tourism

- AI oncology

Threats

- Imported innovation dependence

- Price pressure

- Infrastructure gaps

15. PESTLE Analysis

Political

Government healthcare expansion.

Economic

Growing middle class.

Social

Cancer awareness rising.

Technological

AI and genomics adoption.

Legal

Regulatory strengthening.

Environmental

Pollution-linked burden.

16. Emerging Trends Through 2035

Major shifts expected:

- Immunotherapy expansion

- Biomarker-driven care

- Genomic screening

- AI-enabled diagnostics

- Hospital decentralization

- Home-based supportive oncology

- Digital survivorship

Global oncology growth is expected to remain strong throughout the next decade, supporting India’s trajectory. (Global Market Insights Inc.)

17. Strategic Recommendations

Government

- Expand screening

- Strengthen registries

- Build regional centers

Pharma

- Accelerate oncology pipelines

- Expand biosimilars

Hospitals

- Develop integrated cancer hubs

Investors

- Prioritize precision oncology

Academia

- Increase translational research

Conclusion

India’s oncology market stands at a historic inflection point.

The next decade will determine whether India becomes merely a large consumer of oncology innovation—or emerges as a global architect of affordable, scalable, precision cancer care.

The opportunity extends beyond revenue.

It includes:

- reducing mortality,

- democratizing advanced treatment,

- creating pharmaceutical sovereignty,

- and positioning India as a global oncology leader.

The future of Indian oncology will belong not only to those who invent therapies—but to those who make them accessible, scalable, and clinically meaningful.

Estimated Outlook: India’s oncology ecosystem is entering a prolonged expansion phase with oncology, precision diagnostics, radiation infrastructure, and advanced therapeutics becoming central pillars of healthcare growth through 2035. (IMARC Group)