From Generic Dominance to Innovation Sovereignty: India’s Next Pharmaceutical Revolution

A Detailed Strategic Analysis and Insight Report

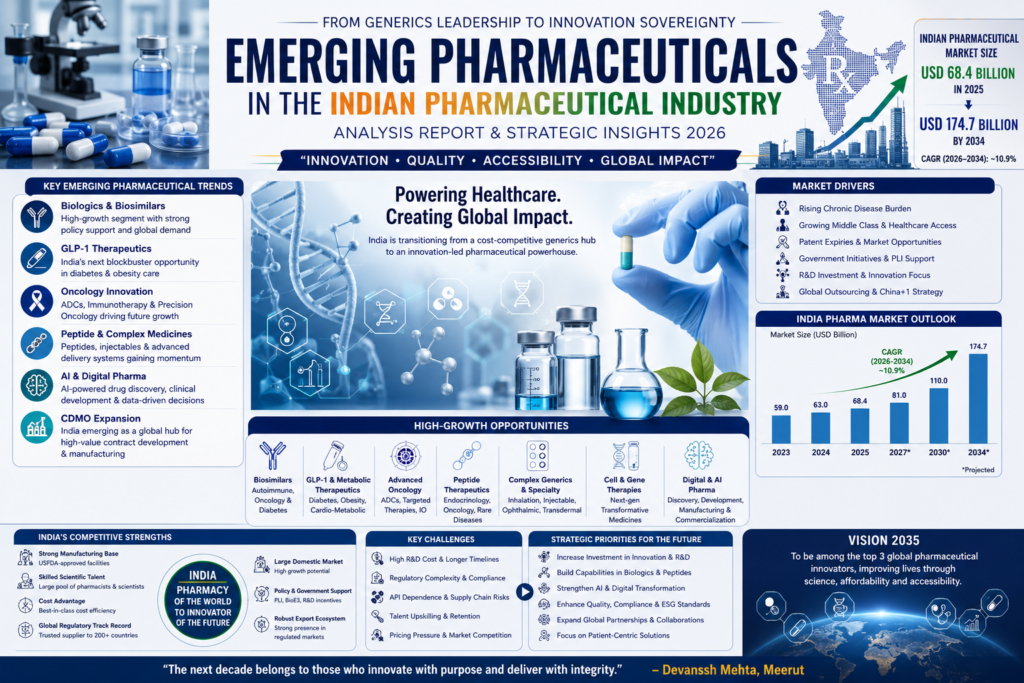

By Devanssh Mehta, Meerut, Uttar Pradesh, India

Executive Summary

India’s pharmaceutical industry is entering one of the most consequential transitions in its modern history.

For decades, India was recognized as the “pharmacy of the world” because of scale, affordability, and manufacturing excellence in generic medicines. That identity remains powerful—but insufficient for the decade ahead.

The year 2026 marks the beginning of a structural shift:

from generic manufacturing → toward innovation-led pharmaceutical value creation.

The emerging pharmaceutical landscape in India is now increasingly shaped by:

- biologics and biosimilars,

- GLP-1 therapeutics,

- peptide medicines,

- oncology innovation,

- complex generics,

- advanced drug delivery systems,

- AI-enabled pharmaceutical R&D,

- CDMO expansion,

- precision medicine,

- digital therapeutics,

- and pharmaceutical sovereignty.

The opportunity is not incremental.

It is transformational.

India’s pharmaceutical market reached approximately USD 68.4 billion in 2025 and multiple forecasts project continued expansion through the next decade with growth approaching USD 174.7 billion by 2034 under sustained innovation and demand expansion. (IMARC Group)

Introduction: The End of the Generic-Only Era

The Indian pharmaceutical industry was built on four historic strengths:

- Process chemistry excellence

- Cost-efficient manufacturing

- Regulatory adaptability

- Global generic supply leadership

But healthcare itself has changed.

Patients increasingly demand:

- targeted therapy,

- personalized treatment,

- superior outcomes,

- convenience,

- reduced toxicity,

- and measurable value.

Traditional blockbuster models are fragmenting.

Therapeutic complexity is increasing.

Drug development is becoming computational.

India’s next competitive advantage will therefore emerge not merely from producing medicines—

but from creating pharmaceutical intelligence.

Recent sector discussions increasingly emphasize India’s transition toward capability-led growth, with biologics, biosimilars, advanced services, and innovation becoming central themes. (The Times of India)

Understanding “Emerging Pharmaceuticals”

Emerging pharmaceuticals are not simply new medicines.

They represent high-value therapeutic and technological categories expected to redefine future healthcare economics.

Major categories include:

First-generation innovation

New molecular entities (NMEs)

Complex pharmaceuticals

Difficult-to-manufacture formulations

Biologics

Large molecule therapeutics

Biosimilars

Comparable biologic alternatives

Peptide therapeutics

Cell and gene therapies

Smart drug delivery systems

AI-supported discovery pipelines

Precision and companion therapeutics

India is now participating across nearly all these layers.

The GLP-1 Revolution: India’s Defining Pharmaceutical Opportunity

If one therapeutic class symbolizes pharmaceutical disruption in 2026—

it is GLP-1.

Originally developed for diabetes management, GLP-1 receptor agonists have rapidly expanded into obesity and metabolic medicine.

The global obesity therapeutics market has entered accelerated expansion, with estimates placing market value near USD 92 billion in 2026, with further long-term growth expected. (IQVIA)

India’s domestic GLP-1 opportunity is becoming increasingly strategic.

Industry estimates cited by CareEdge indicate India’s GLP-1 segment—valued around ₹1,000–1,200 crore in 2025—could expand toward ₹4,500–5,000 crore by 2030. (eHealth Magazine)

Patent transitions and increasing competition are accelerating Indian entry into this category. (India Briefing)

Recent launches indicate commercial momentum has already begun in India’s metabolic innovation landscape. (The Times of India)

Strategic implications

GLP-1 is not merely another drug class.

It represents:

- peptide manufacturing maturity,

- biologics capability,

- device integration,

- chronic-care economics,

- and long-duration patient engagement.

Biologics and Biosimilars: India’s Second Pharmaceutical Independence

Small molecules built India.

Biologics may define its future.

Biologics now represent one of the fastest-growing pharmaceutical categories worldwide.

India’s industry leadership increasingly recognizes that the future growth engine lies in:

- biosimilars,

- specialty medicines,

- advanced manufacturing,

- and platform capabilities. (The Times of India)

Recent market outlooks identify biologics and biosimilars as the fastest-growing molecular segment in India, despite conventional small molecules remaining dominant today. (Grand View Research)

Budget and policy support have strengthened this direction.

The 2026 policy framework announced a ₹10,000-crore multi-year push toward biologics and biosimilars manufacturing capability. (The Economic Times)

Areas expected to dominate:

- autoimmune disorders,

- oncology,

- diabetes,

- hematology,

- inflammatory disease.

Oncology Pharmaceuticals: India Moves Toward High-Value Cancer Medicine

Cancer care is becoming one of the most sophisticated pharmaceutical battlegrounds.

Emerging oncology categories include:

Antibody–Drug Conjugates (ADCs)

Combining selective antibody targeting with cytotoxic potency.

Immuno-oncology

Activating endogenous immune mechanisms.

Precision Oncology

Biomarker-driven therapy selection.

High-Potency APIs (HPAPIs)

Advanced manufacturing for oncology pipelines.

Modern oncology manufacturing increasingly requires specialized CDMO infrastructure capable of handling complex molecules and accelerated development pathways. (Pinnacle Life Science)

For India, oncology is strategically important because it combines:

- scientific complexity,

- export value,

- and clinical demand.

Complex Generics: India’s Silent Competitive Weapon

A major misconception in pharmaceutical analysis is that generics are finished.

They are evolving.

Complex generics include:

- liposomal drugs,

- inhalation products,

- depot injections,

- transdermals,

- combination therapies,

- ophthalmic systems.

Industry assessments increasingly identify complex generics and biosimilars among the strongest growth themes beyond 2026. (India Pharma Outlook)

Complexity creates margins.

Margins create reinvestment.

Reinvestment creates innovation.

Peptide Medicines: The New Frontier

Peptides may become one of India’s most strategically important pharmaceutical segments.

Drivers include:

- diabetes,

- obesity,

- endocrinology,

- oncology.

India is actively preparing manufacturing capability in:

- peptide synthesis,

- biologics processing,

- advanced APIs,

- global compliance systems. (LinkedIn)

The next pharmaceutical manufacturing race may not be antibiotics.

It may be peptide scalability.

CDMO Transformation: Manufacturing Becomes Intellectual Infrastructure

Contract Development and Manufacturing Organizations (CDMOs) are evolving.

Traditional outsourcing focused on cost.

Next-generation outsourcing prioritizes:

- scientific capability,

- quality,

- regulatory sophistication,

- speed.

India’s biopharmaceutical and CDMO ecosystem is increasingly benefiting from:

- outsourcing demand,

- China+1 supply-chain diversification,

- biologics manufacturing,

- specialty production expansion. (Kalkine)

This transition may significantly elevate India’s position from manufacturing destination to development partner.

Artificial Intelligence and the New Pharmaceutical Architecture

AI is becoming the operating system of pharmaceutical innovation.

Applications include:

Drug Discovery

Molecule prediction.

Clinical Development

Protocol optimization.

Manufacturing

Predictive quality systems.

Pharmacovigilance

Signal detection.

Commercial Intelligence

Demand forecasting.

Industry leaders increasingly view AI as capable of materially reducing pharmaceutical development timelines and operational cost structures. (The Times of India)

Future pharmaceutical organizations may operate as:

Bio + Data + Manufacturing + AI ecosystems.

Market Outlook: Indian Pharma Beyond 2026

Current industry estimates suggest:

- Indian pharmaceutical market value reached approximately USD 68.38 billion in 2025. (IMARC Group)

- Forecast growth approaches 10–11% CAGR over the coming decade depending on methodology. (IMARC Group)

- Domestic market growth in FY27 is expected near 9%, supported by launches and pricing expansion. (www.pharmabiz.com)

Strategic growth pillars:

| Segment | Strategic Momentum |

|---|---|

| Generics | Stable |

| Complex Generics | High |

| Biosimilars | Very High |

| GLP-1 | Explosive |

| Oncology | High |

| CDMO | Accelerating |

| Digital Pharma | Emerging |

| Precision Medicine | Early but Strategic |

Risks That India Must Solve

Despite optimism, structural constraints remain.

Regulatory Complexity

Global scrutiny continues to intensify.

Quality Variability

Operational discipline remains essential.

R&D Funding Gap

Long innovation cycles require patient capital.

API Dependence

Supply-chain resilience remains strategic.

Talent Conversion

Scientific education must align with translational capability.

Recent analyses continue to identify compliance pressure, export dependence, and supply-chain resilience among key determinants of competitiveness. (DrugPatentWatch)

Strategic Outlook: What Will Define Winners?

The next pharmaceutical champions in India will likely demonstrate:

- biologics capability,

- regulatory excellence,

- AI integration,

- advanced manufacturing,

- therapeutic specialization,

- clinical evidence generation.

The winners of 2035 may not necessarily be the largest manufacturers.

They may be those who learn fastest.

Conclusion: India Is No Longer Competing Only on Cost

The future of Indian pharmaceuticals is not a story of cheaper medicines.

It is a story of smarter medicines.

The industry is entering an era where molecules will compete not only on efficacy—

but on intelligence, manufacturability, accessibility, and evidence.

India has already proven it can supply the world.

The question for the coming decade is larger:

Can India discover, design, manufacture, and lead the medicines that define the future of humanity?

2026 suggests the answer may increasingly become—

yes.

— Devanssh Mehta, Meerut